It can be tough to decide about the loan. Another drawback is the rates of interest on the loan might be high depending upon your credit. Knowing the fundamental truths can avoid "What is reverse home loan confusion.' Nevertheless, you do need to be familiar with all possible situations. For instance, you may encounter a scenario where the individual who signed the reverse home mortgage goes into a retirement home while his spouse remains at home.

It is necessary to comprehend the risks and to have a strategy I place in case the worst possible scenario happens. You can lower the risk by limiting the amount you borrow on the loan (how do buy to rent mortgages work). If it is a small part of the total equity, you can offer the home and have enough to buy a smaller location live.

It can help you preserve your self-reliances and fix a capital problem if your retirement benefits are unable to cover all of your costs. Many federal government firms are alerting elders to carefully evaluate the terms and consider all choices prior to taking out a reverse mortgage. Home loan statistics show that if you borrow money versus your home, you do have an opportunity of losing the home, however if you do not put the home up as security, you do not have the exact same danger.

The monetary outlook for America's aging population can seem pretty bleak. More than 40% of baby boomers have no retirement cost savings, according to a research study from the Insured Retirement Institute. Of the boomers who did handle to conserve for retirement, 38% have less than $100,000 leaving much of them without the cash they'll require.

Getting The How Do Reverse Annuity Mortgages Work To Work

Well-meaning grandparents who guaranteed on student loans to assist their children or grandchildren defray the costs of college successfully increased their own student loan debt concern from $6. 3 billion in 2004 to $85. 4 billion in 2017. Nevertheless, there is a silver lining to https://www.businesswire.com/news/home/20200115005652/en/Wesley-Financial-Group-Founder-Issues-New-Year%E2%80%99s this sobering story. Baby boomers own 2 out out every 5 homes in the U.S., with an estimated $13.

The equity in these homes might be sufficient to bridge the cost savings gap and reduce the debt burden by allowing elders to access their home equity through a home mortgage product called a reverse home loan. House cost increases given that 2012 are providing more accessible equity for seniors in requirement of the flexibility of the reverse home mortgage program to resolve present monetary issues, or avoid them from happening in the future.

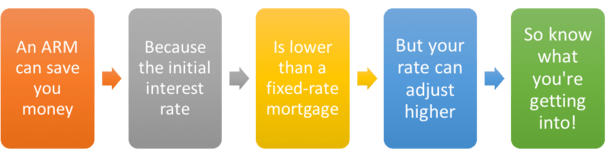

In this article, we will cover: A traditional home loan needs a regular monthly payment of principal and interest, and is often called a "forward home mortgage." The whole quantity is borrowed in one swelling sum and is paid "forward" on a fixed regular monthly payment schedule till the balance is down to absolutely no.

Your balance increases over time as you access the equity accumulated in your home. After examining just how much equity remains in your home, a reverse home loan lender will give you money in a lump sum, as regular monthly income or a combination of both. You can utilize all of the equity you're authorized to borrow simultaneously, or demand a line of credit to access later.

Getting The How Do Buy To Rent Mortgages Work To Work

Interest is contributed to the balance you borrow each month on a reverse home loan, while the quantity of equity you have shrinks. Reverse home mortgages aren't right for everybody, however there are a number of financial objectives you might have the ability to achieve by taking out one. If you are on a set income, decreasing your month-to-month costs will provide you room in your budget to feel more comfortable about spending your money.

If your existing set earnings is insufficient for you to reside on conveniently, a reverse home loan can supplement your income. As you age, it can become harder to do home upkeep, and if you have any specials needs you may be confronted with choices about assisted living. A reverse home mortgage might provide you the extra cash required to pay for home-care, or for specialists to assist keep your home maintained and safe for you to live in.

Nevertheless, take care before signing for a reverse home loan. Nearly 10% of reverse mortgage customers in the HECM program lost their houses to reverse mortgage foreclosures https://www.prweb.com/releases/2012/8/prweb9766140.htm in between 2006 and 2011. As an outcome, new policies were taken into place that require a conference with an HUD-certified counselor prior to using for any reverse mortgage item.

The therapist will discuss your financial requirements, and provide you with objective feedback about how a reverse home mortgage can and can't satisfy those requirements. "Consumers require to make sure that a reverse home mortgage is a sustainable option for their monetary circumstances," stated Steve Irwin, executive vice president of the National Reverse Home Loan Lenders Association.

Some Ideas on What Can Itin Numbers Work For Home Mortgages You Should Know

You can use a reverse home loan calculator to identify your eligibility. The older you are, the more you are usually permitted to obtain. The standard requirements to receive a reverse mortgage are listed below: At least one borrower must be 62 or older. You need to own the house you are financing, free and clear of any loans, or have a substantial quantity of equity.

The residential or commercial property you are funding should be your primary house. You can't be delinquent on any federal debt. Documents needs to be provided revealing sufficient income or properties to cover the payment of your residential or commercial property taxes and property owners insurance. Because you do not make a payment on a reverse home mortgage, there is no escrow account established to pay your typical housing-related expenditures.

The approval procedure for a reverse home loan resembles getting any other type of mortgage. Submit a loan application, provide documents as requested by your lending institution, get an appraisal on your home and title work that verifies you have appropriate ownership, and after that you close. There is one additional step you'll require to take previously you request a reverse mortgage: For a lot of reverse home loans, it's compulsory to meet an HUD-approved housing therapist prior to application and offer evidence of that conference to your loan provider.

The FHA increased the loan limitation on its reverse home loans from $679,650 to $726,525. This indicates that people with high-value houses will have the ability to gain access to more of their equity. "That's excellent news for consumers who have homes that have increased in value," Irwin said. There are likewise a variety of new proprietary reverse home loan programs being offered in 2019, Irwin stated.

Our How Do Construction Mortgages Work Statements

These programs have loan amounts up to $6 million that will offer a chance for customers to access the equity in properties at high-cost parts of the nation. For consumers thinking about reverse home loans who have not quite reached the minimum age requirement of 62, a new proprietary item will enable reverse home loan funding for debtors as young as 60 years of ages - how do mortgages payments work.

A lot of these condos are in buildings that not authorized by the FHA, so they are not able to pursue the reverse home mortgage choices provided by the federally-insured reverse home mortgage. Proprietary home loan lending institutions now provide loan programs that will provide condominium owners reverse home loan funding options that are not possible within the constraints of the FHA condo-approval procedure.